.jpg)

The Age Pension, a significant source of income for many Australian retirees, has seen a boost as of 20th March 2024. The maximum full Age Pension has increased by $19.60 per fortnight for a single person and $29.40 for a couple combined.

The Age Pension, a significant source of income for many Australian retirees, has seen a boost as of 20th March 2024. The maximum full Age Pension has increased by $19.60 per fortnight for a single person and $29.40 for a couple combined. This increase, although modest, is a welcome relief for many.

The increase in the Age Pension base rate and main supplement is based on a Consumer Price Index (CPI) increase of 1.8%, which was higher than the increase in the Pensioner and Beneficiaries Living Cost Index (PBLCI) that rose by 1.5% over the past six months.

Services Australia uses different economic indicators to measure price and wage increases and then apply this movement to keep Age Pensioners ‘in touch’ with the working population. This indexation takes place twice a year, on 20 March and 20 September.

The three key components of indexation are:

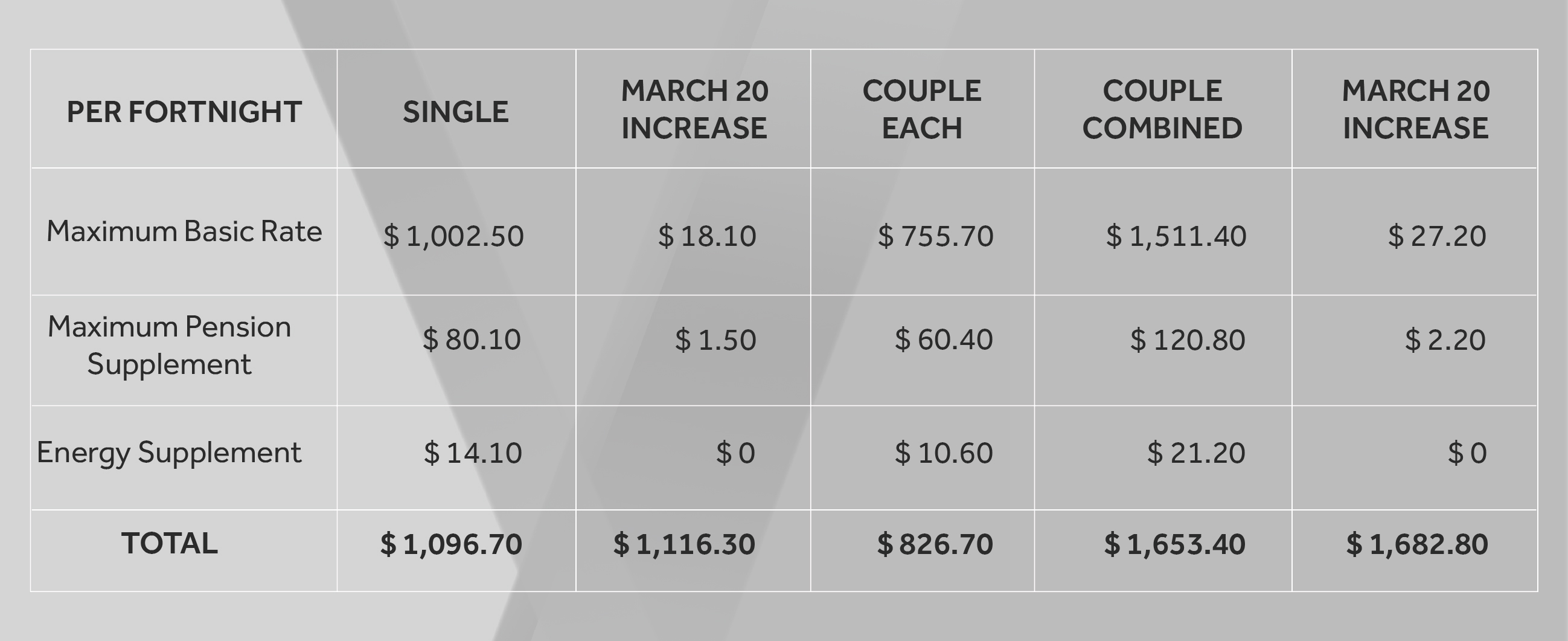

The new rates for a full Age Pension for Australian residents for the period 20 March 2024 to 19 September 2024 are as follows:

The question remains, is this enough? The CPI is the determinant, in theory, the Age Pension increase should cover your own personal cost of living increases caused by higher prices for goods and services. But is the extra $10 or $15 per week really enough? In your experience, have the costs of those items that your household consumes only gone up by 1.8%? It seems unlikely when we think about things like fuel, insurances and supermarket shopping.

We’d love to hear your thoughts on whether the expected increase will help to cover price increases – or if it’s two cups of coffee a week and not much more?

Shortly after Services Australia officially announces the 20 March indexation changes, the Retirement Essentials Age Pension Entitlements Calculator will be updated to reflect the new amounts. In the meantime, it can be used for free to assist with all your calculations on the current rates.

If you are approaching the time when you apply for an Age Pension or you wish to review the amount you are currently receiving, a Maximising Your Entitlements consultation will allow you to fully understand all the entitlements strategies at your disposal.

Despite the growth in superannuation over the past three decades, the Age Pension is still a significant source of income for most Australian retirees. According to Rice Warner, roughly 39% of Australians of Age Pension age receive the full Age Pension and a further 24% receive a part pension.

So how much income does the Age Pension provide? From 20 March 2024 the maximum full Age Pension increases $19.60 per fortnight for a single person, and $14.70 per person per fortnight for a couple.

The Age Pension rates will potentially change on 20 September 2024. Increases are likely but not certain because the Australian Bureau of Statistics evaluates these increases based on changes in the Consumer Price Index (CPI), Male Total Average Weekly Earnings, and the Pensioner and Beneficiary Living Cost Index. In September 2020 the Age Pension rates did not increase, although that was for the first time since 1997.

To qualify for the Age Pension in Australia you must have reached Age Pension age (which depends on your date of birth but is now 67), satisfy Australian residency rules, and pass both an income test and an assets test. Depending on your level of income and the assets you own, you may qualify for either a full or part Age Pension.

Assets test: To qualify for a full Age Pension as a single person your assets must also be valued below $301,750 if you own your own home, or $543,750 if you don’t own your own home. You can still be eligible for a part Age Pension if your assets are worth less than $674,000 if you own your own home, or $916,000 if you don’t own your own home.

Income test: To qualify for a full Age Pension as a single person your income must be below $204 per fortnight (approximately $5,304 per year), but you can still be eligible for a part Age Pension if you earn less than $2,436.60 per fortnight (approximately $63,352 per year).

For a couple, to qualify for the full Age Pension your combined income must be below $360 per fortnight (approximately $9,360 per year), but you can still be eligible for a part Age Pension if you earn less than $3,725.60 per fortnight (approximately $96,866 per year).

It’s important to note that you can earn up to $300 per person per fortnight (up to $11,800 per year) from working and this amount is not included in the Age Pension income test. This is known as the work bonus.

If you are over the threshold limits for a full Age Pension in either the assets or income tests (or both), your Age Pension will be based on the test that delivers the lower amount. For example, if you are eligible for $400 per fortnight according to the assets test, and $500 per fortnight through the income test, then the assets test ($400 per fortnight) will apply.

What happens if only one member of a couple is eligible? This is a common question. If you’re in a living arrangement with your partner and only one of you is eligible for the Age Pension, do you receive the single rate or half of the combined couple rate?

The answer is you will be assessed under the income and assets tests as a couple and, if eligible, you will receive half the combined couple rate. This is best illustrated with an example.

Example: Bill reached his Age Pension eligibility age of 67 years in January 2024. He meets the Age Pension residency requirements and passed both the assets and income tests, not reaching the lower thresholds of either one. He is therefore eligible for the maximum Age Pension. However, his partner Sue is only 62 and she is therefore not yet old enough to be eligible for the Age Pension. Using the Age Pension rate table provided above, Bill would be entitled to the maximum Age Pension of $841.40 for each eligible person in a couple living arrangement.

Bill would also be entitled to the maximum pension supplement of $61.50. He would not be eligible for the energy supplement because this is only available for people who had a Commonwealth Seniors Health Card before 20 September 2016.

If you receive the Age Pension, you’ll automatically be paid a pension supplement. You’ll receive the maximum rate if you’re eligible to receive the full pension, but if you’re only eligible for a part pension (for example if your income or assets exceed the thresholds in the Age Pension income or assets tests), your pension supplement will be reduced proportionally until it reaches the minimum amount.

You can arrange to have the pension supplement paid quarterly rather than fortnightly if you prefer, to help you budget for regular quarterly bills like electricity.

Markets continue to experience uncertainty as global events, interest rate decisions, and geopolitical developments influence investor sentiment. In this market update, Tyson Roberts provides insights into recent market movements, including oil price shifts, central bank decisions, inflation concerns, and the importance of maintaining a diversified investment approach during changing conditions.

Understanding changes to superannuation rules can help Australians make more informed retirement decisions. In this article, Kate Borch explains what the new $3 million super tax may mean, why strategic planning is important, and the opportunities available to help structure super balances effectively while preparing for the future.

Preparing for retirement involves more than just knowing your super balance — it’s about creating a clear plan for the years ahead. In this article, Sonia Mezentseff explains the key steps to consider before retirement, including understanding your income needs, reviewing your super, planning for entitlements, organising important documents, and designing the lifestyle you want for your next chapter.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.