.jpg)

Last week, the government implemented adjustments to the stage three tax cuts, which were originally introduced by the previous Liberal government.

Last week, the government implemented adjustments to the stage three tax cuts, which were originally introduced by the previous Liberal government. These changes aim to deliver more equitable financial relief, particularly targeting low and middle-income earners who have been disproportionately impacted by the rising cost of living. Initially heavily skewed towards high-income individuals, the revised plan strives to distribute benefits more fairly across the income spectrum.

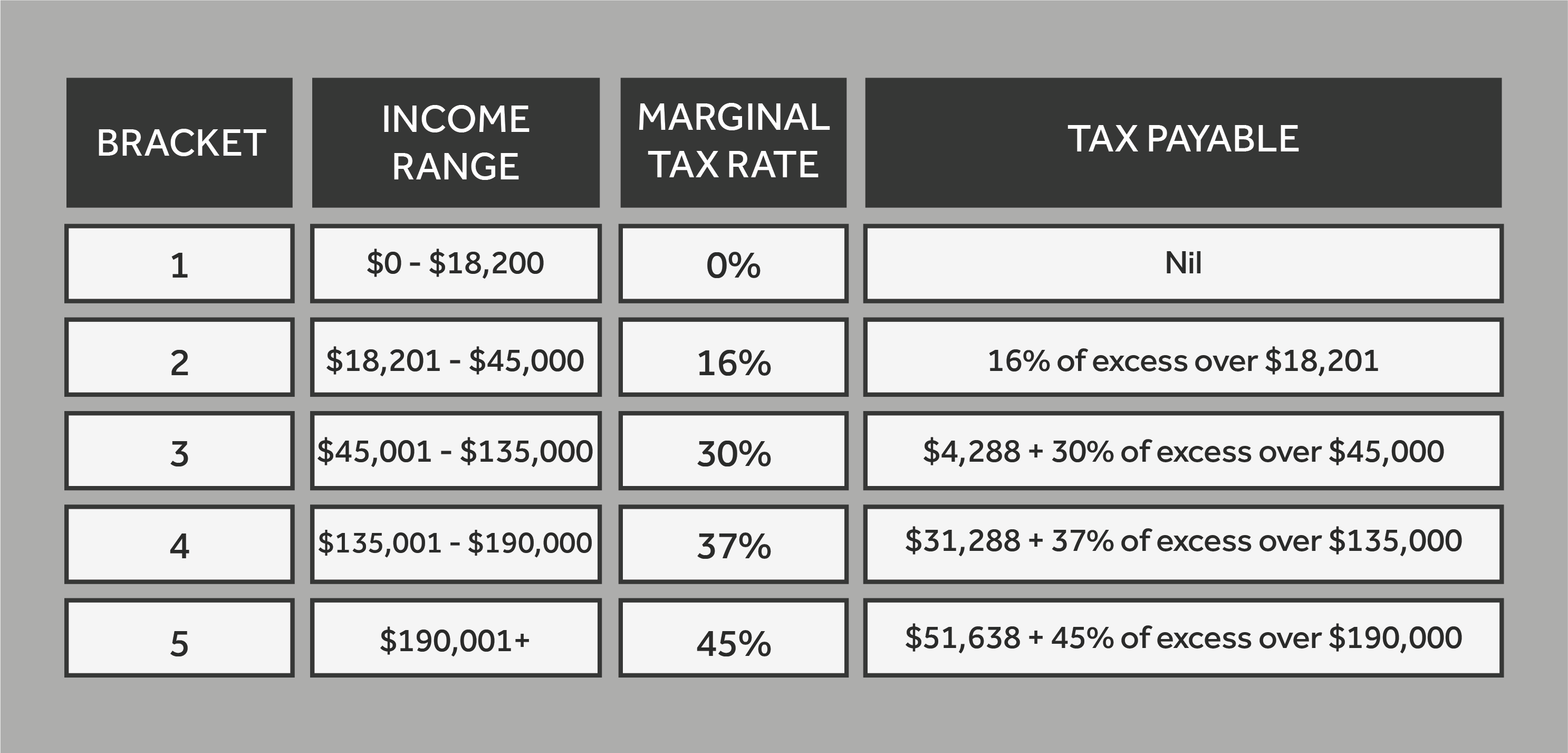

The Income Tax System Before Stage 3 Tax Cuts

Prior to the stage three tax cuts, Australia's income tax system consisted of four tax brackets:

For instance, someone earning $50,000 per year would pay:

Original Stage Three Tax Cuts

The original stage three tax cuts were set to take effect on July 1, 2024. The key changes included eliminating the 37% marginal tax rate for those earning more than $120,000 per year and reducing the 32.5% tax rate to 30% for incomes between $45,000 and $200,000. This would create a single 30% tax bracket for individuals earning between $45,000 and $200,000, with the 45% rate remaining for incomes above $200,000.

However, this plan primarily benefited high-income earners:

Adjusted Tax Cuts

The redesigned stage three tax cuts introduce several notable changes:

Under the new scheme, high-income earners will see reduced benefits. For example, an individual earning $200,000 will now save $4,546 instead of $9,075.

Updated Tax Brackets from July 1, 2024

The revised tax brackets are:

Medicare Low-Income Threshold Adjustment

Additionally, the Medicare low-income threshold will be increased. The Medicare levy, which is 2% of taxable income, is exempted for low-income earners. For the 2024-25 year, individuals earning $26,000 or less will be exempt from paying the Medicare levy. The levy gradually increases after this threshold, with the full 2% paid by those earning more than $32,500. This adjustment represents a 7.1% increase from the 2023-24 thresholds, aligning with inflation.

Redistribution of Tax Benefits

The overall cost of the tax cuts remains unchanged, but the savings are now more evenly distributed. Low and middle-income earners, who previously received minimal benefits, will now see more significant relief. The table below highlights the redistribution of tax cuts:

The stage three tax cuts have been restructured to provide more equitable benefits across various income levels. The initial plan heavily favoured high-income earners, while the revised cuts offer substantial relief to low and middle-income Australians who have faced rising living costs. These changes ensure a fairer distribution of tax savings, supporting a broader segment of the population during challenging economic times. Understanding these adjustments allows taxpayers to better plan their finances and make informed decisions about their economic future.

Global markets are entering the second half of 2026 amid shifting economic conditions, cooling AI momentum and lower oil prices. Tyson Roberts explores the key trends shaping investment markets, where new opportunities may be emerging, and why diversification remains essential in an evolving investment landscape.

Major changes to SMSF property investing are coming from 10 August 2026. New legislation will prevent SMSFs from entering into new borrowing arrangements to purchase residential property, while existing loans are expected to be protected.

July 2026 Centrelink changes could improve Age Pension eligibility for some retirees. While the increased assets and income thresholds may allow more people to qualify for a part pension, the actual benefit depends on whether your entitlement is assessed under the assets or income test. If you're close to the eligibility limits, now may be the right time to review your Centrelink position and ensure you're receiving any benefits and concessions available to you.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.