.jpg)

Retirement planning is a multifaceted endeavour that often centres around the pivotal question: "How much do I need to retire?"

While many immediately turn to their superannuation savings for an answer, the complexity of this query extends beyond the mere accumulation of assets. In this article, we will delve into why retirement planning is fundamentally an income question, shedding light on factors such as lifestyle, investment returns, government support, and other considerations that may affect the overall retirement landscape for Australians.

For those seeking retirement planning Melbourne guidance, understanding how income, lifestyle, and long-term financial goals work together is an essential part of building a sustainable retirement strategy.

The traditional approach to retirement planning often centres on the accumulation of a substantial nest egg. However, experts argue that this perspective oversimplifies the intricacies of retirement planning. It's not merely about the size of your nest egg; it's about ensuring a sustainable income stream that supports your desired lifestyle.

One key consideration is the assumption that retirees own their homes. The figures mentioned earlier, such as the AFCA Retirement Standard and the safe super drawdown rate of 5% per annum, presume that accommodation costs are minimal. If retirees need to factor in rent, the income requirements could be higher, making it crucial to tailor retirement plans to individual circumstances.

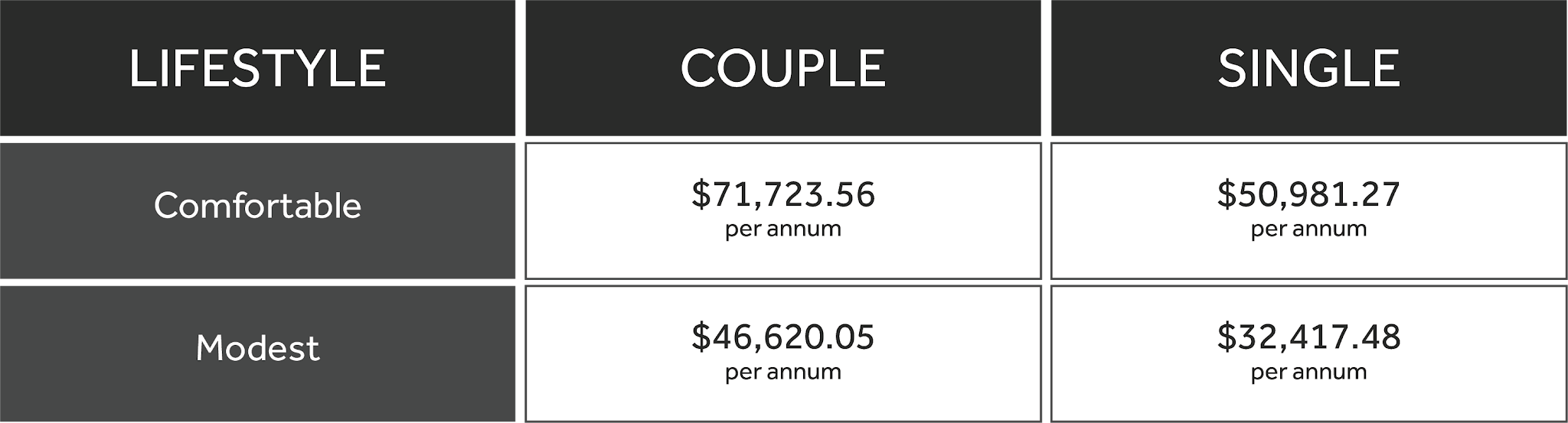

To provide a more tangible understanding of retirement income needs, financial planners often refer to standards set by the Australian Financial Complaints Authority (AFCA). As of today's date, AFCA suggests that for a comfortable lifestyle, a couple would need $71,723.56 annually, while a modest lifestyle requires $46,620.05. For a single person, the figures are $50,981.27 for a comfortable lifestyle and $32,417.48 for a modest lifestyle.

Let's break down this information in a concise table, keeping in mind that these figures presume homeownership:

In the challenging landscape of retirement income, the government's support through the Age Pension, administered by Centrelink, serves as a stark reality check. While the full Age Pension currently amounts to $1,096.70 per fortnight for a single person and $826.70 per fortnight for each member of a couple, it's disheartening to note that these figures fall significantly short of the AFCA Retirement Standard.

Considering the AFCA's recommendation of $32,417.48 per annum for a modest lifestyle for singles and $46,620.05 per annum for a couple, the annual Age Pension payments add up to $28,514.00 for singles and $42,988.00 for couples. The glaring shortfall is undeniable, emphasising the harsh reality that even the modest lifestyle benchmark remains out of reach for those relying solely on the Age Pension. This underscores the importance of strategic financial planning, as it's clear that government support alone may not suffice for many Australians aiming for a comfortable retirement.

Speaking with a retirement planner Melbourne based professional can help individuals better understand how superannuation, investments, and government support may work together to fund retirement income needs.

While the AFCA Retirement Standard provides a baseline, it's essential to acknowledge that it doesn't account for lump-sum expenses that retirees might incur during their golden years. Purchases such as a new car, dream holidays, or unexpected medical expenses can impact the overall retirement budget. Additionally, market fluctuations can influence investment returns, altering the anticipated income and, consequently, the financial outlook for retirees.

For many Australians, seeking retirement advice Melbourne can help uncover potential gaps in retirement income planning and prepare for unexpected costs later in life.

When planning for retirement, a holistic perspective becomes indispensable. Beyond considering superannuation and government support, individuals must account for potential lump-sum expenses, the impact of market fluctuations, and, in the case of non-homeowners, rental costs.

Financial planners play a pivotal role in guiding individuals through this intricate process. They assess current financial situations, estimate future expenses, and develop personalised plans that align with retirement goals. By incorporating a comprehensive understanding of income needs, retirees can make informed decisions that account for the dynamic nature of their retirement years.

Accessing retirement planning advice Melbourne can provide greater clarity around long-term income strategies and help retirees feel more confident about their financial future.

In conclusion, the question of "How much do I need to retire?" transcends the simplicity of an account balance. It's about ensuring a steady income that accommodates your chosen lifestyle throughout retirement, accounting for nuances such as homeownership, potential lump-sum expenses, and market fluctuations. Collaborating with a financial planner becomes paramount, as they can help tailor strategies to individual circumstances, providing a roadmap to a retirement that is not only financially secure but also aligned with personal aspirations.

Retirement planning is a dynamic process that requires adaptability, ensuring a comfortable and fulfilling retirement journey. Whether you're just beginning to explore retirement planning Melbourne strategies or reviewing your existing plan, taking a proactive approach today with Vista Financial can make a meaningful difference to your long-term financial security.

Markets continue to experience uncertainty as global events, interest rate decisions, and geopolitical developments influence investor sentiment. In this market update, Tyson Roberts provides insights into recent market movements, including oil price shifts, central bank decisions, inflation concerns, and the importance of maintaining a diversified investment approach during changing conditions.

Understanding changes to superannuation rules can help Australians make more informed retirement decisions. In this article, Kate Borch explains what the new $3 million super tax may mean, why strategic planning is important, and the opportunities available to help structure super balances effectively while preparing for the future.

Preparing for retirement involves more than just knowing your super balance — it’s about creating a clear plan for the years ahead. In this article, Sonia Mezentseff explains the key steps to consider before retirement, including understanding your income needs, reviewing your super, planning for entitlements, organising important documents, and designing the lifestyle you want for your next chapter.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.