.jpg)

The recent market correction has understandably raised concerns among clients about the future direction of the market.

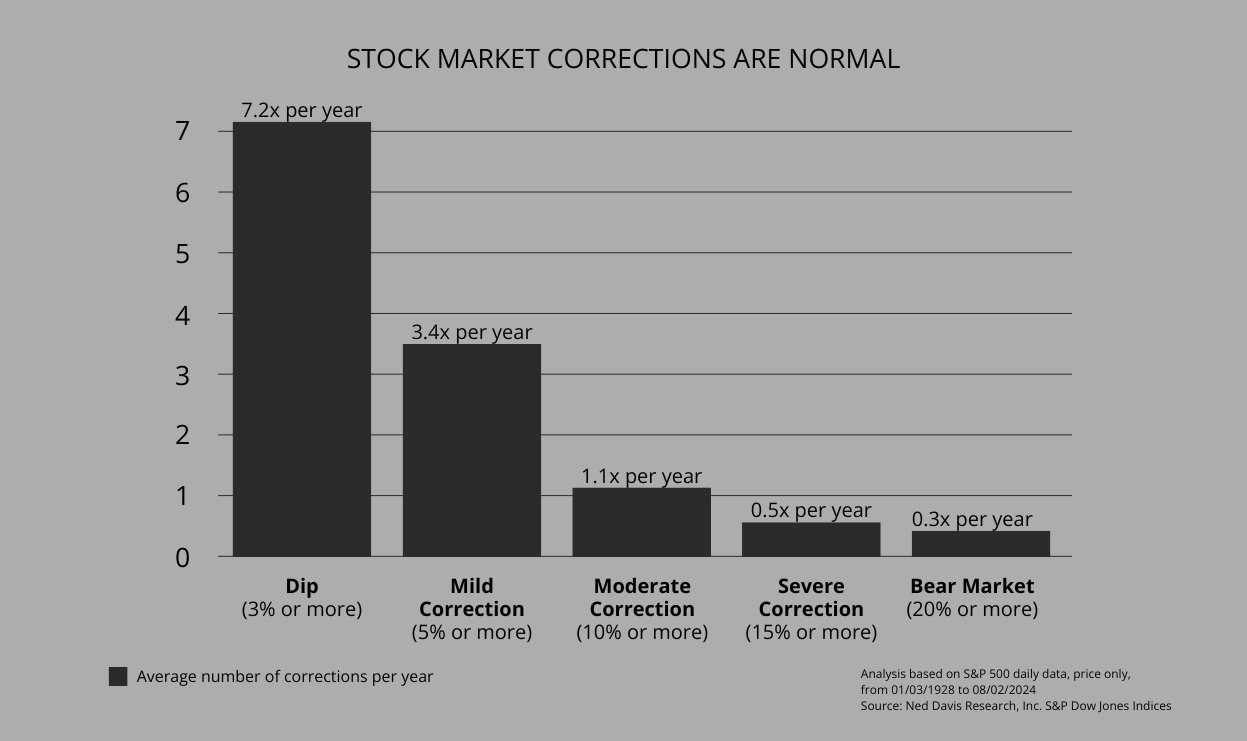

The recent market correction has understandably raised concerns among clients about the future direction of the market. At Vista Financial Group, we strive to take emotion out of the equation and rely on data-driven insights to guide our investment strategies. It's important to remember that market corrections are a normal occurrence, with an average of one 10% correction happening each year.

Economic Outlook and Indicators

Despite the recent market turbulence, there is no strong evidence pointing towards an impending recession. Only one out of ten indicators in our Recession Watch Report is negative. We are seeing currently projections of a real GDP growth of 1.5% to 2.0% for this year. A balanced approach shows some negative price-driven indicators for stocks and bonds, but external indicators remain positive. These price-driven indicators are likely to revert if the market rally resumes.

Our analysis also shows that the market is already oversold. The Daily Trading Sentiment Composite has entered the extreme pessimism zone. Historically, when this composite falls to 20 or below, the S&P 500 has seen an 80% probability of rising by a median of 3.8% one month later. Currently, the composite stands at 31.1, indicating a potential for positive movement ahead.

Japanese Market Dynamics

The Japanese market has been particularly volatile, with the yen's momentum no longer supporting the market. However, we believe this won't trigger a global risk-off scenario. Once the current sell-off subsides, we expect the global uptrend to resume. It's important to stay focused on long-term strategies and avoid making hasty decisions based on short-term market fluctuations.

Predicting short-term market movements is inherently challenging due to the volatility we are experiencing. However, our indicators suggest that a recovery is more probable than a continued decline. This view is supported by recent market behavior. For instance, after a significant 12% drop on Monday, Japan's Nikkei rebounded by 10% on Tuesday. Similarly, US equity futures indicated a higher opening by about 0.75% as of 8 AM. The recent sell-off has left the S&P 500 in extremely oversold territory, which typically precedes a period of mean reversion and potential gains.

US Market

The S&P 500 rose by 54 points overnight, a 1.0% increase to 5,240, rebounding from sharp declines over the previous three sessions. Investors targeted undervalued stocks, with the Real Estate sector performing the strongest, up by 2.3%. The yield on the US 10-year treasury increased by 10 basis points to 3.89%, while the US Dollar Index rose by 0.3% to $102.97.

In terms of trade, the US trade deficit in international goods and services narrowed from $75.0 billion in May to $73.1 billion in June, aligning with market expectations. This reduction in the trade deficit is a positive sign for the economy.

Australian Market

The ASX 200 climbed 31 points, closing 0.4% higher at 7,681, recovering from two heavily sold-off sessions. The Consumer Discretionary sector led the gains, rising by 1.6%, with six out of eleven sectors ending in positive territory. The SPI Futures Index, however, was trading 19 points lower at 7,615 this morning. The yield on the 10-year treasury fell by 3 basis points to 4.02%, and the AUDUSD increased by 0.3% to 0.6520.

In corporate news, Treasury Wine Estates Limited (TWE) provided a FY24 earnings update, with unaudited EBITS expected to be $658.1 million, up 13% year-on-year. TWE announced a non-cash impairment charge of $290 million after tax for its Treasury Premium Brands division and plans to divest its Commercial brand portfolio. TWE shares rose by 1.0%, closing at $11.70.

Audinate Group Limited (AD8) reported unaudited FY24 results, showing a revenue of approximately US$60 million, up 28% from the previous year, and expected EBITDA in the range of AUD19.5-$20.5 million, compared to AUD$11 million in the previous year. Despite this growth, AD8 gave a cautious FY25 outlook due to anticipated revenue challenges and headwinds, leading to a projected decline in FY25 before a return to growth in FY26. As a result, AD8 shares fell by 36.3%, closing at $8.48.

The Reserve Bank of Australia (RBA) held interest rates steady at 4.35% during their recent meeting, as expected. The RBA remains cautious about inflation, which is still above the 2-3% target range, due to persistent service costs. They have not ruled out further rate hikes if inflation risks remain elevated.

ASX 200 Top Movers

ASX 200 Bottom Movers

while recent market volatility has created uncertainty, our data-driven approach indicates a likely recovery rather than a prolonged downturn. It's crucial to maintain a long-term perspective and stay informed through reliable indicators and market analysis. At Vista Financial Group, we are committed to guiding our clients through these turbulent times with sound advice and strategic insights.

Global markets are entering the second half of 2026 amid shifting economic conditions, cooling AI momentum and lower oil prices. Tyson Roberts explores the key trends shaping investment markets, where new opportunities may be emerging, and why diversification remains essential in an evolving investment landscape.

Major changes to SMSF property investing are coming from 10 August 2026. New legislation will prevent SMSFs from entering into new borrowing arrangements to purchase residential property, while existing loans are expected to be protected.

July 2026 Centrelink changes could improve Age Pension eligibility for some retirees. While the increased assets and income thresholds may allow more people to qualify for a part pension, the actual benefit depends on whether your entitlement is assessed under the assets or income test. If you're close to the eligibility limits, now may be the right time to review your Centrelink position and ensure you're receiving any benefits and concessions available to you.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.