.jpg)

When it comes to planning for retirement, many Australians focus heavily on the accumulation phase making regular contributions to their superannuation and watching it grow over time. However, the real challenge begins once retirement hits.

When it comes to planning for retirement, many Australians focus heavily on the accumulation phase making regular contributions to their superannuation and watching it grow over time. However, the real challenge begins once retirement hits. Transitioning from accumulating wealth to managing it effectively during retirement is crucial, yet it’s an aspect that often goes overlooked.

The Importance of Staying Invested in Retirement

As you approach retirement, it’s tempting to adopt a conservative approach, shifting your superannuation into low-risk, cash-based investments. While this might seem like the safest option, it could potentially cost you in the long run. The reality is that living longer and facing inflation means your retirement savings need to work harder for you, even after you’ve stopped working.

Australia’s life expectancy continues to rise, with many retirees living well into their 80s and beyond. This extended lifespan means your retirement funds need to last longer. If your investments are too conservative, you risk depleting your savings too quickly, especially as inflation erodes the purchasing power of your money over time.

For instance, consider two retirees with $1,000,000 in superannuation at age 65. If one adopts a highly conservative approach, allocating 100% of their portfolio to cash with an annual return of 2%, and the other opts for a balanced portfolio with a mix of growth assets (returning 6% annually) and defensive assets (returning 3% annually), the difference in their account balances at age 80 could be substantial. The conservative portfolio might grow to only $1,268,241, while the balanced portfolio could reach $2,086,755, highlighting the long-term benefits of staying invested in a diversified portfolio.

Understanding Inflation and Its Impact

Inflation is a critical factor to consider in retirement planning. It’s the gradual increase in the cost of goods and services, which can significantly impact your retirement savings. For instance, what costs $100 today could cost much more in 20 or 30 years. If your retirement portfolio is too heavily weighted in cash or low-yield investments, the returns may not keep pace with inflation, diminishing your purchasing power over time.

To illustrate this, let’s look at the historical average inflation rate in Australia, which has been around 2.5% per annum. If you retire today with $1,000,000 and withdraw $50,000 annually, assuming a 2% return on cash investments, your purchasing power would significantly diminish over a 20-year retirement period. By the end of that period, the $50,000 you withdraw would only have the purchasing power equivalent to about $30,000 today. In contrast, a diversified portfolio with an average return of 6% could help maintain your purchasing power by providing the potential for growth that outpaces inflation.

The Risk of Being Too Conservative

While it’s natural to want to protect your nest egg by moving to safer investments, this strategy can backfire. A portfolio that’s too conservative may not generate enough growth to sustain you throughout retirement. This is especially true in today’s low-interest-rate environment, where returns on cash and bonds are minimal. In contrast, a balanced approach that includes a mix of growth and defensive assets can provide the potential for both capital preservation and growth.

For example, a balanced superannuation option that includes a diversified mix of growth assets, such as equities, and defensive assets, like bonds, can help manage risk while still offering the potential for growth. Over time, this approach may provide better outcomes than a purely conservative strategy, especially when it comes to keeping up with inflation.

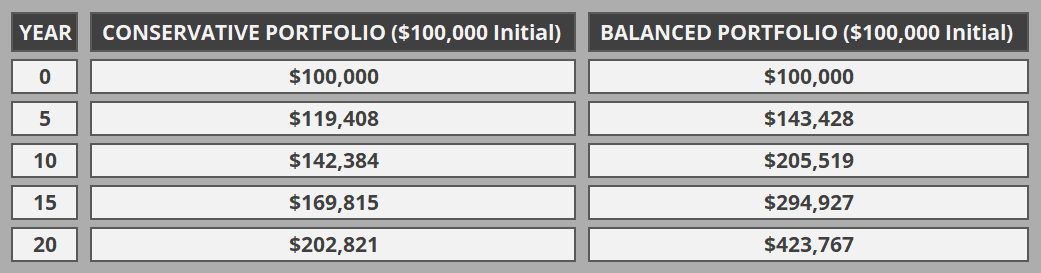

Conservative vs. Balanced Portfolio Growth Over 20 Years

In this scenario, the conservative portfolio grows at a steady rate of 3.5% per year, reflecting a low-risk investment strategy. The balanced portfolio, with a mix of growth and defensive assets, assumes a 7.5% annual return. Over 20 years, the balanced approach significantly outperforms the conservative one, highlighting the potential benefits of staying invested in growth assets even during retirement.

Managing Market Volatility in Retirement

Market volatility is another concern for retirees, particularly when it comes to withdrawing funds from their super during a downturn. However, history has shown that markets tend to recover over time. By staying invested in a well-diversified portfolio, you can ride out short-term fluctuations and benefit from the long-term growth potential of your investments.

One effective strategy is to maintain a cash reserve or "bucket" within your retirement portfolio. This reserve can cover your living expenses for a few years, allowing you to avoid selling growth assets during a market downturn. By keeping this buffer, you give your other investments time to recover and continue growing, which can significantly improve your financial security in retirement.

The Importance of Tailored Financial Advice

Every retiree’s situation is unique, and there’s no one-size-fits-all approach to managing your super in retirement. That’s why it’s essential to seek tailored financial advice that takes into account your personal circumstances, including your risk tolerance, income needs, and other assets.

A financial adviser can help you develop a retirement strategy that balances the need for growth with the desire for security. They can also assist in navigating complex issues like social security, tax implications, and potential legislative changes that could affect your retirement planning.

While it’s important to protect your retirement savings, being overly conservative can lead to unintended consequences, such as outliving your money or losing purchasing power due to inflation. By staying invested in a diversified portfolio and seeking professional advice, you can better manage the risks associated with retirement and enjoy the financial security you’ve worked so hard to achieve.

At Vista Financial Group, we’re here to help you navigate these challenges and ensure your retirement is everything you’ve dreamed of. Whether you’re just entering retirement or already enjoying it, our team of experts can provide the guidance and support you need to make informed decisions about your financial future.

Global markets are entering the second half of 2026 amid shifting economic conditions, cooling AI momentum and lower oil prices. Tyson Roberts explores the key trends shaping investment markets, where new opportunities may be emerging, and why diversification remains essential in an evolving investment landscape.

Major changes to SMSF property investing are coming from 10 August 2026. New legislation will prevent SMSFs from entering into new borrowing arrangements to purchase residential property, while existing loans are expected to be protected.

July 2026 Centrelink changes could improve Age Pension eligibility for some retirees. While the increased assets and income thresholds may allow more people to qualify for a part pension, the actual benefit depends on whether your entitlement is assessed under the assets or income test. If you're close to the eligibility limits, now may be the right time to review your Centrelink position and ensure you're receiving any benefits and concessions available to you.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.