.jpg)

From 1 July 2026, super contribution caps will increase, creating new opportunities for concessional, non-concessional and bring-forward contributions — but also introducing updated thresholds and planning considerations. With higher limits and expanded eligibility, forward strategy will be key to maximising contributions and avoiding costly missteps as retirement approaches.

What’s changing for super contribution caps and bring forward provisions from 1 July 2026?

The release of February’s AWOTE figures results solidifies an increase to the concessional contributions cap, which will rise to $32,500 from 1 July 2026 (up from $30,000 in 2025/26). Additionally, the non-concessional contributions cap will also increase to $130,000. These updated contribution limits, along with the revised transfer balance cap, will also mean changes to the table of thresholds relevant for bring forward contributions.

New Concessional and Non-Concessional contribution limits and thresholds

From 1 July 2026, we will see increased cap availability for the 2026/27 FY:

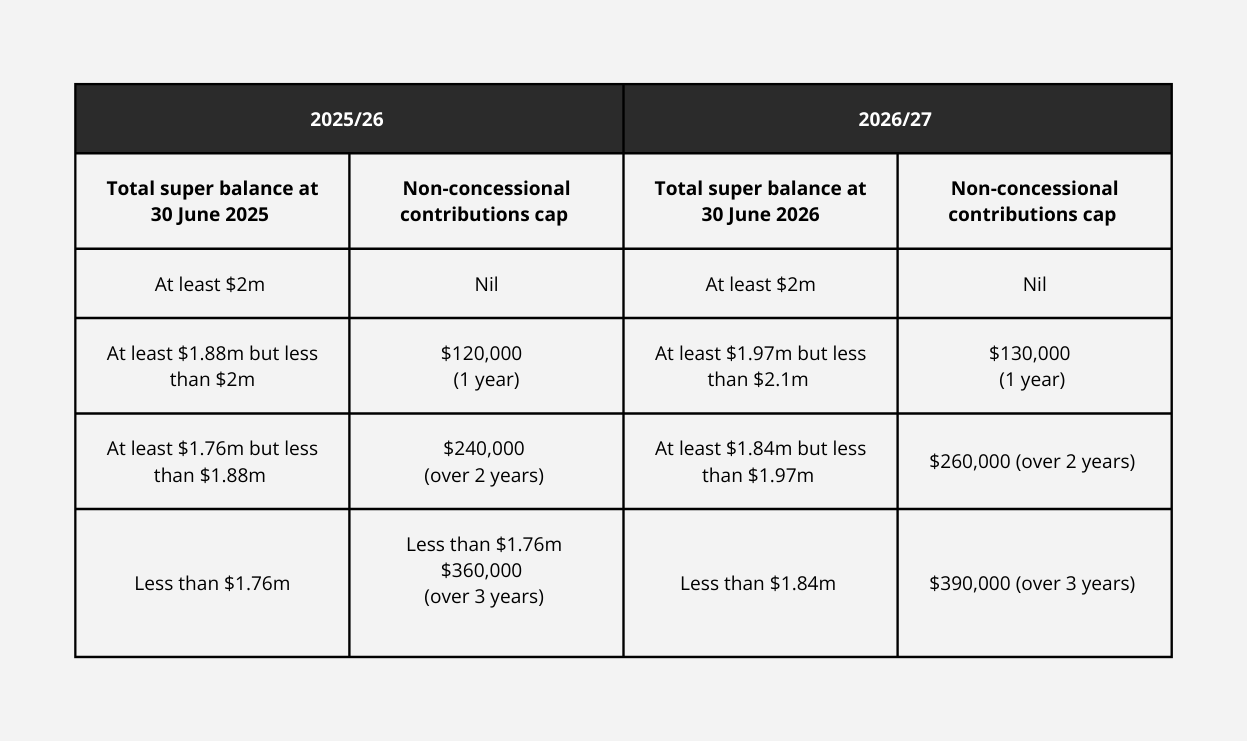

New bring forward thresholds for 2026/27

The "bring forward rules" represent an important consideration for individuals seeking to increase their superannuation balances as retirement approaches. Key questions are often:

The new table for 2026/27 will look much different to the current FY:

This table has changed significantly in recent years. In 2021/22, having $1.8m in super meant no non-concessional contributions could be made without exceeding the threshold ($1.7m).

Previously, bring forwards were only allowed up to age 67, but now they're possible until age 75. For details on rules near age 75 we suggest discussing your individual circumstances.

With the caps lifting and opportunities being greater, contribution planning is particularly noteworthy this year.

Strategic contribution opportunities

When change occurs in and around superannuation, if often presents extra emphasis on forward planning. In this instance, the level of contributions you can make in the remaining part of 2025/26 is likely to be quite different to what you will be able to contribute from 1 July 2026.

Some key questions you should be considering:

Understanding the changes can be one thing, applying them to your own financial position can be another. We are here to help you navigate the questions above if you need a hand optimising your retirement planning.

Global markets are entering the second half of 2026 amid shifting economic conditions, cooling AI momentum and lower oil prices. Tyson Roberts explores the key trends shaping investment markets, where new opportunities may be emerging, and why diversification remains essential in an evolving investment landscape.

Major changes to SMSF property investing are coming from 10 August 2026. New legislation will prevent SMSFs from entering into new borrowing arrangements to purchase residential property, while existing loans are expected to be protected.

July 2026 Centrelink changes could improve Age Pension eligibility for some retirees. While the increased assets and income thresholds may allow more people to qualify for a part pension, the actual benefit depends on whether your entitlement is assessed under the assets or income test. If you're close to the eligibility limits, now may be the right time to review your Centrelink position and ensure you're receiving any benefits and concessions available to you.

Stay in the know with the latest updates, insights, and exclusive content delivered straight to your inbox.